Law of Demand and Supply

What is Demand?

Demand, in the context of economics, refers to the quantity of goods and services that a consumer is willing and able to buy.

Determinants of Demand

The demand for a particular commodity in an economy depends on several factors, such as:

- Price of the commodity.

- Price of the other related goods.

- Income of consumers.

- Tastes and preferences of consumers.

- Size of the market i.e. the number of consumers, etc.

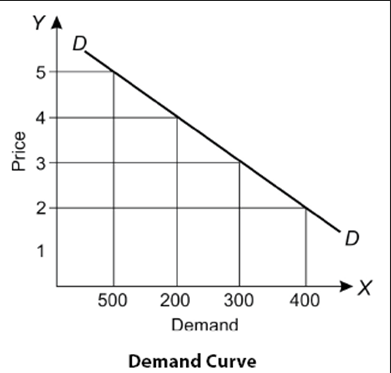

Demand Curve

- Demand Curve is the graphical representation of the relationship between the price of a commodity and the quantity of the commodity demanded.

- The independent variable (Price) is represented along the Y-axis and the dependent variable (Quantity) is represented along the X-axis.

- The demand curve, usually, moves downward from the left to the right.

Income Effect and Substitution Effect

Income Effect

The income effect represents the change in an individual’s or economy’s income and its impact on the quantity demanded of a good or service. Usually, with an increase in income, an individual demands more goods and services, other things remaining constant.

Substitution Effect

The substitution effect occurs when a consumer replaces one commodity with another due to a change in relative prices and/or personal income. This includes replacing cheaper items with those more expensive, or vice versa.

Difference between Income Effect and Substitution Effect

The income effect refers to a change in demand for a commodity due to a change in income. The substitution effect, on the other hand, shows the change in demand for a product due to a relative change in price and the availability of substitutable products.

The prominence of these effects, usually, depends on the market scenario as can be seen as follows:

- In a market with few choices or substitutes, a rise in the price of a commodity may show the income effect more prominently.

- In such a scenario, consumers may stop buying the commodity altogether.

- In a market with multiple substitution options, a rise in the price of a commodity may show the substitution effect more prominently.

- In such a scenario, consumers can choose to buy a similar but more affordable product.

Law of Supply and Demand Defined

You're about to launch a new product, but you aren't sure how much to produce or how much to charge. Price it too high or make too much of it, and you could be left with unsold stock. If you price too low or don't make enough, you'll lose potential profit. Everything depends on the demand for the product — how much customers will buy at what price. That's why the law of supply and demand is so relevant to business decisions. It predicts the relationship between supply, demand and pricing. Understanding the law of supply and demand can help businesses meet customer demand while maintaining healthy profits and minimizing excess stock.

What Is the Law of Supply and Demand?

The law of supply and demand is the theory that prices are determined by the relationship between supply and demand. If the supply of a good or service outstrips the demand for it, prices will fall. If demand exceeds supply, prices will rise.

The law of supply and demand is based on two other economic laws: the law of supply and the law of demand. The law of supply says that when prices rise, companies see more profit potential and increase the supply of goods and services. The law of demand states that as prices rise, customers buy less.

Theoretically, a free market will move toward an equilibrium quantity and price where supply and demand intersect. At that point, supply exactly matches the demand — suppliers produce just enough of a good or service, at the right price, to satisfy everyone's demands.

Key Takeaways

- The law of supply and demand predicts that if the supply of goods or services outstrips demand, prices will fall. If demand exceeds supply, prices will rise.

- In a free market, the equilibrium price is the price at which the supply exactly matches the demand.

- Understanding the law of supply and demand helps businesses determine how to set prices and fulfill customer demand while minimizing excess inventory.

Law of Supply and Demand Explained

The law of supply and demand describes how the relationship between supply and demand affects prices. If a supplier wants more money than the customer is willing to pay, items will most likely stay on the shelf. If the price is set too low, customers will be eager to buy the items, but each item will be less profitable. The law of supply and demand is based on the interaction between two separate economic laws: the law of supply and the law of demand. Here's how they work.

The Law of Supply.

The law of supply predicts a positive relationship between pricing and supply. As prices of goods or services rise, suppliers increase the amount they produce — as long as the revenue generated by each additional unit they produce is greater than the cost of producing it. Seeing a greater potential for profits, new suppliers may also enter the market. For example, prices of lithium and other metals used in batteries have soared as sales of electric vehicles have increased. That has encouraged mining companies to explore new sources of lithium and expand production at existing mines in order to increase the supply and generate higher profits.

The law of supply can also operate on a local scale. Let's say a well-known musician is coming to town. Anticipating a huge demand for tickets, promoters aim to maximize the supply by booking the biggest venue possible and offering as many tickets as they can, at high prices. As the supply of tickets runs out, the price of secondhand tickets rises — and so does the supply — as casual fans who bought tickets at the list price see the opportunity to resell them at a higher price. As a result, they enter the market as new suppliers.

The Law of Demand.

The law of demand says that rising prices reduce demand. So as prices rise, customers buy less. That's particularly true if they can substitute cheaper goods. When the famous musician comes to town, not everyone may be able to afford a ticket even if they'd like to go. So, if the theater sets prices too high, fewer people will decide it's a worthwhile purchase, and the show organizers will be left with empty seats. Fans who want to resell their tickets may need to lower their asking price. Some people may decide to see another artist instead, if those tickets are cheaper.

Assumptions to Law of Demand

The demand for a commodity depends on multiple factors and not just the price. However, in order to put things simply, the Law of Demand makes some assumptions as explained below:

- Income of the consumer remains constant: Usually, the demand for a particular commodity increases with the increase in income of the consumer and vice versa. This, in turn, can affect the demand curve. However, the Law of Demand assumes that the income of the consumer remains constant for the time being.

- Tastes and preferences of the consumer don’t change: A change in taste and preference of the consumer in favor of a particular commodity, usually, increases the demand for that commodity and vice versa. However, the Law of Demand assumes that for the time being the taste and preference of the consumer remains constant.

- Size and composition of population remain constant: An increase/decrease in population would increase/decrease the number of consumers and hence increase/decrease the demand for a particular commodity. Similarly, any change in the composition of the population means that the needs of the population change and so does the demand for the commodity. Hence, the Law of Demand assumes that these two population variables remain constant.

Exceptions to the Law of Demand

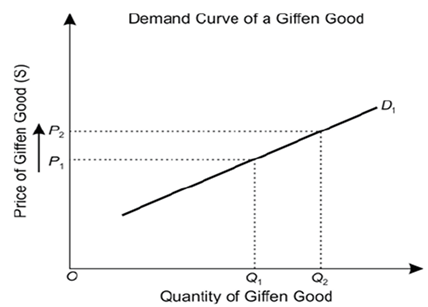

Giffen Goods

- A Giffen good is a good for which demand increases as the price increases, and falls when the price decreases. Thus, for a Giffen good, the demand curve is an upward-sloping demand curve, which is contrary to the Law of Demand.

- A Giffen good is typically an inferior good that does not have easily available substitutes. Thus, in this case, the income effect dominates the substitution effect.

- Staple foods are an example of Giffen Goods.

- They are consumed by poor people who are unable to afford superior foods.

- As the price of superior foods increases, they become unaffordable to more people, who then resort to Giffen Goods. Thus, demand for Giffen Goods (staple food) increases.

Veblen Goods

- A good for which demand increases as the price increases, because of its exclusive nature and appeal as a status symbol. Thus, just like Giffen goods, the demand curve for Veblen goods is upward-sloping, which is contrary to the Law of Demand.

- However, unlike Giffen goods, a Veblen good is generally a high-quality, coveted product.

The Law of Supply and Demand.

The price where supply and demand meet is known as the equilibrium price. At that price point, suppliers produce just enough of a good or service to satisfy demand, and everyone who wants to purchase the product can do so. In practice, of course, balancing supply and demand is more complex. As supply and demand fluctuate, the equilibrium price can vary over time. Furthermore, the law of supply and demand assumes that all other factors that can affect pricing remain constant. In reality, that's often not the case. For example, fluctuating production costs or supply chain problems can have a big impact on pricing.

Why Is the Law of Supply and Demand Important?

Business success in any competitive market depends on accurately assessing supply and demand. Every company that launches a new product needs to determine how much of the product to make and how much to charge. A business that manufactures too much of a product or sets prices higher than customers will pay can easily find itself left with products that don't sell and become dead stock. On the other hand, understocking or setting prices too low reduces profits and can drive away customers who can't wait for backorders to be fulfilled. Demand forecasting can help businesses determine the optimal supply level and find the equilibrium price — the price at which the supply just meets customer demand.

4 Basic Laws of Supply and Demand

The law of supply and demand predicts four ways that changes in either demand or supply will drive changes in pricing:

- Prices fall when supply increases and demand remains constant.

- Prices fall when demand decreases and supply remains constant.

- Prices rise when supply decreases and demand remains constant.

- Prices rise when demand increases and supply remains constant.

If supply increases without a change in demand, a surplus usually occurs. This can happen for many reasons, including surges in productivity. To move excess stock, especially if there's a pending expiration date, suppliers tend to lower prices to try to boost demand.

A surplus can also occur when customers want less of a good or service, even without a change in supply. The effect is the same: lower prices.

If supply drops, shortages occur. In that situation, customers are often willing to pay higher prices to get the goods and services they want. Supply constraints can occur for many reasons, including supply chain problems. If the problem is temporary, prices tend to return to their baseline once supply is restored.

A shortage can occur if the demand for a product increases but the supply doesn't — or if demand increases faster than production can ramp up. When supply eventually catches up with demand, prices tend to stabilize.

| Supply | Demand | Inventory Level | Price Change |

|---|---|---|---|

| Increases | Remains constant | Surplus | Lower |

| Remains constant | Decreases | Surplus | Lower |

| Decreases | Remains constant | Shortage | Higher |

| Remains constant | Increases | Shortage | Higher |

How changes in supply and demand affect prices and supplier inventory.

Demand Curve

A demand curve is a graph that tracks the relationship between price (vertical axis) and demand (horizontal axis). The downward slope indicates that when prices rise, demand tends to fall.

The extent to which price changes affect demand varies from product to product. For any product, the steepness of the curve is a measure of its demand elasticity — the extent to which demand is affected by changes in the price. A less steep curve indicates that a small change in price causes a large change in demand.

Note that the demand curve only considers the effect on demand of a single factor — price. Other factors that influence demand, such as advertising, can shift the entire demand curve to the left or right.

Supply Curve

A supply curve shows the relationship between price (vertical axis) and supply (horizontal axis). It indicates how much output suppliers are willing to produce at different prices. When a supplier sees more profit potential from higher prices, it often will allocate more of its resources toward those more profitable items — usually at the expense of lower-priced items. At the same time, newcomers may enter the market, further increasing the available supply — because with the promise of higher revenue, more companies may be prepared to invest the startup costs required to enter that market.

Like demand curves, supply curves consider the effect of pricing but assume that everything else remains constant. However, other factors, such as production costs, can affect the supply. For example, if rising hamburger prices are dictated by more expensive beef, a restaurant owner may not see enough profit from the higher prices and may not have much incentive to expand capacity by adding another grill to the kitchen. Other constraints, such as limits on manufacturing capacity or the availability of raw materials, may also negatively impact the ability to increase supply.

Balance Between Supply and Demand

Understanding the balance between supply and demand is critical in many industries. Price is a key factor in determining this balance — although it's not the only factor. The extent to which price affects demand depends on the type of product being sold. It also depends on the competitiveness of the market. For some nonessential goods or items with many available substitutes, there will be high demand elasticity — and demand for one of those products will be highly affected by price changes. In contrast, demand for essential goods, like gasoline or health care, is relatively inelastic: If someone needs gas to get to work, they will probably pay for it no matter the price, especially if they don't have other options, like public transit.

Many other factors can affect the balance between supply and demand, thus impacting pricing. For example, supply can be affected by the cost of raw materials, technology that increases productivity, transportation or other supply chain issues, and government regulations.

Law of Supply and Demand Examples

Simple Supply and Demand Example: Croissants

| Component | Scenario | Supply & Demand Relationship |

|---|---|---|

| Normal Day | The bakery typically bakes 50 croissants and sells them all by noon. They charge 260.00 each. | The quantity supplied (50) is roughly equal to the quantity demanded at this price, suggesting a near equilibrium. |

| Increased Demand | A local food blogger features the croissants, causing a huge spike in popularity. Customers line up and all 50 are sold out by 8:00 AM. Many potential customers leave disappointed. | Demand has increased significantly more than the current supply. The price will likely rise in the short term, and the bakery will see an opportunity to increase supply (bake more) to meet the new demand. |

| Increased Supply/Oversupply | To meet the new demand, the bakery starts baking 100 croissants. However, a new, trendy coffee shop opens nearby and takes away some customers. Now, they only sell 70 croissants per day. | Supply now exceeds demand at the current price of 260.00. The remaining 30 croissants will be excess inventory. The bakery might respond by lowering the price (e.g., a "two-for-one" special in the late afternoon) or reducing the number they bake the next day to better match demand. |

This simple example shows the constant tug-of-war:

- High Demand + Low Supply = Higher prices and an incentive for producers to increase supply.

- Low Demand + High Supply = Lower prices and an incentive for producers to decrease supply.

Better Supply and Demand Planning With NetSuite

Net Suite Supply and Demand Planning helps businesses balance supply and demand to ensure that they can fulfill customer orders while minimizing excess inventory. Part of an integrated suite of business applications, Net Suite Supply and Demand Planning helps increase forecast accuracy, improve product availability, minimize inventory carrying costs and reduce production delays. Net Suite Demand Planning predicts inventory needs, based on factors such as historical demand, seasonality, growth and profit opportunities and sales forecasts. Net Suite Supply Planning helps companies determine how best to meet that demand, generating production and purchasing schedules and creating the relevant work orders and purchase orders.

Conclusion

The law of supply and demand can provide a useful model for understanding and determining pricing. It can help determine an equilibrium price, where suppliers can meet demand without overstocking, and customers get everything they need at a price they can accept. However, supply, demand and pricing can also be influenced by factors that the law of supply and demand doesn't consider, such as production costs, supply chain problems and regulations.

Copyright © 2026 Manupatra. All Rights Reserved.

Toll Free No : 1-800-103-3550

Toll Free No : 1-800-103-3550 +91-120-4014521

+91-120-4014521